Originally designed to ease the financial burden of special occasions like Christmas or birthdays, buy now pay later (BNPL) has evolved into a more contentious offering. While the product continues to assist those facing financial constraints, emerging research reveals a darker side to the BNPL market. By offering predominantly no/low interest loans, BNPL providers have taken advantage of one of society’s failings, specifically overconsumption.

The UK’s Lending Standards Board (LSB) highlights significant knowledge gaps among BNPL users. According to its findings, only half of consumers are aware of the late payment fees associated with BNPL products, leaving many unknowingly exposed to mounting repayment fees and further debt. Furthermore, LSB survey findings also discovered that 36% of BNPL users decide to use the service impulsively at the checkout stage, reflecting the normalisation of compulsive spending in today’s consumer-driven culture.

Go deeper with GlobalData

GlobalData Buy Now Pay Later Analytics 2024

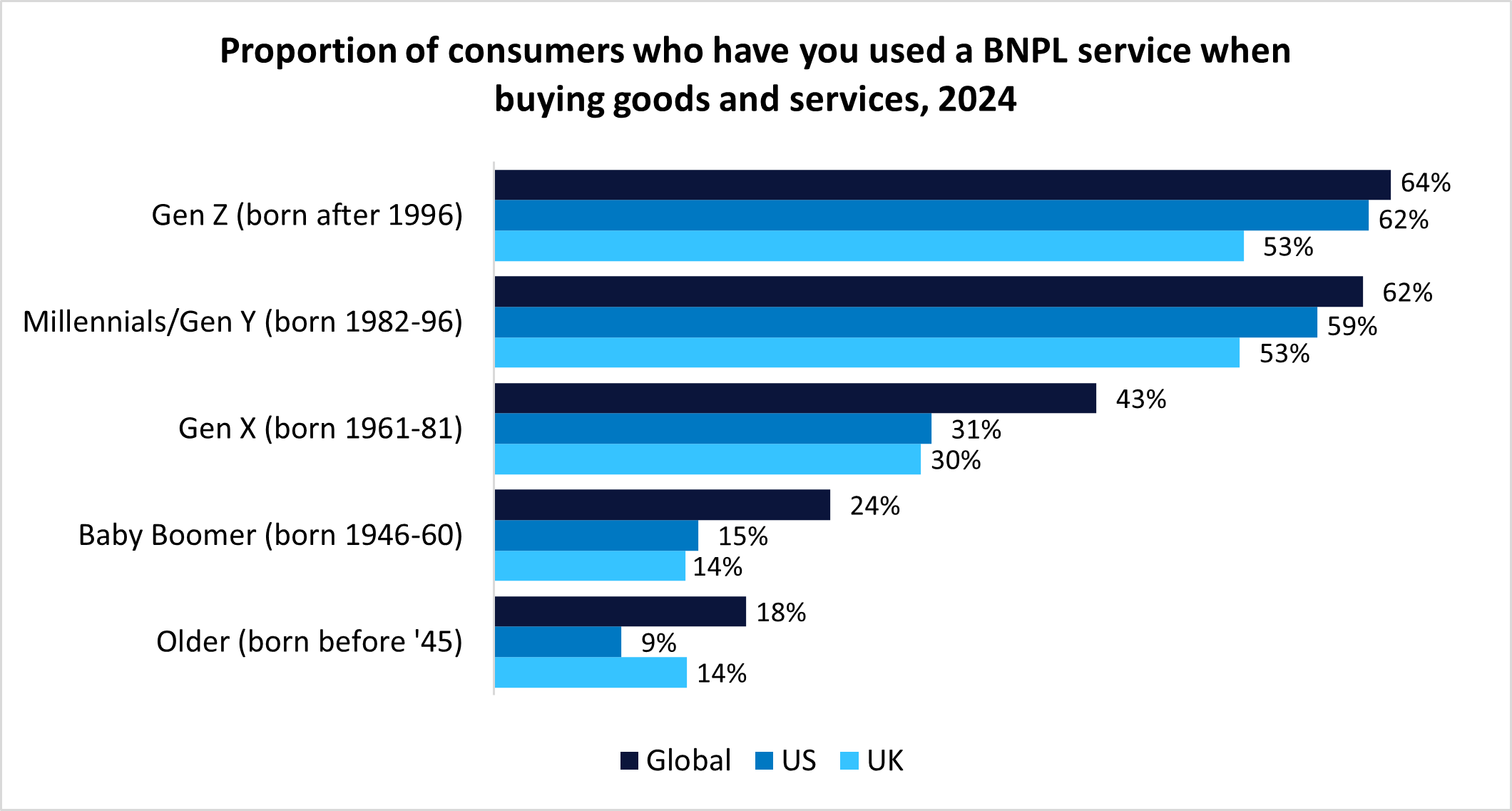

According to GlobalData’s Buy Now Pay Later Analytics 2024, younger generations such as Gen Z are much more likely to use BNPL services than their older counterparts, which is unsurprising considering this is a generation heavily influenced by online trends and influencers. The majority of BNPL transactions fall within the $21–100 range, indicating purchases like non-essential food (takeout meals), clothes, makeup, electronic gadgets, and shoes. The societal pressure to keep consuming is driving unhealthy spending habits, with BNPL platforms enabling impulsive purchases that frequently come with hidden fees. For many younger users, this translates into accumulating debt and, in some cases, diminished credit scores—consequences that can have long-lasting financial repercussions.

Source: GlobalData

The US’s Consumer Financial Protection Bureau (CFPB) report data mirrors the LSB’s findings, with the CFPB noting that “nearly two thirds of BNPL loans went to borrowers with lower credit scores,” including those categorised as subprime or deep subprime credit scores. With minimal protections in place, consumers already struggling in debt are being drawn further into financial hardship. This issue is particularly concerning for Gen Z, where a considerable proportion are still under the age of 18. For these young consumers, who often lack financial responsibilities or experience, debt at such an early stage can set a precarious foundation. BNPL providers are continuing to exploit both those already in debt but also youngsters who do not understand the repercussions of missing repayments.

How well do you really know your competitors?

Access the most comprehensive Company Profiles on the market, powered by GlobalData. Save hours of research. Gain competitive edge.

Thank you!

Your download email will arrive shortly

Not ready to buy yet? Download a free sample

We are confident about the unique quality of our Company Profiles. However, we want you to make the most beneficial decision for your business, so we offer a free sample that you can download by submitting the below form

By GlobalDataBNPL regulation overdue

BNPL regulations in the UK are long overdue and are still not expected to be implemented until 2026 at the earliest. In the meantime, financial education and budgeting have become topical, with many providers producing innovative products designed to boost their customers’ financial knowledge and wealth. Whether these efforts stem from genuine concern or are simply ESG-driven initiatives to improve their reputations, these products are being offered and should be taken advantage of by Gen Z. However, consumers themselves must take some responsibility. Breaking the cycle of trend-driven spending, practicing better budgeting, and thoroughly understanding the financial products they are using are critical steps to mitigating the risks of BNPL.

Until meaningful regulation comes into play, education is key to understanding the pros and cons of using BNPL. Banks, in particular, should take the lead in equipping young consumers with the knowledge to navigate BNPL responsibly, safeguarding not only their financial futures but also banks’ future clientele from being burdened with poor financial habits and debt.

Phoebe Hodgson is an analyst, banking and payments, GlobalData