Germany has a strong economy and high levels of financial inclusion, despite a strong consumer inclination for cash for most transactions.

A popular German maxim is geld stinkt nicht (money does not stink), and consumers still see cash as the best option, due to ingrained habits and a preference for spending within one’s means.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

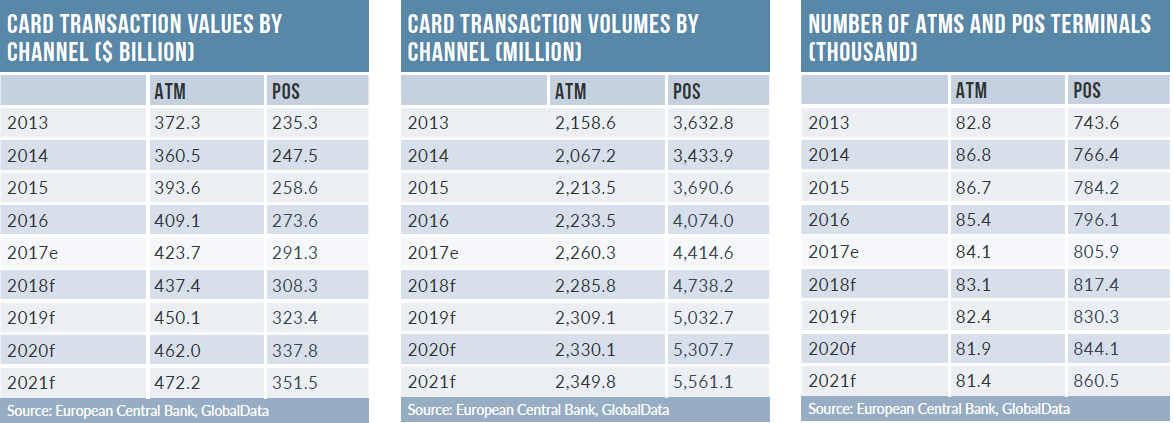

In terms of number of cards in circulation, the German payment card market is third-largest among its peers, behind only the US and the UK, but is still far from recognised as a fully mature market. The average number of monthly consumer card transactions in Germany was 2.4 in 2017, much lower than France (12.4), Canada (9.0) and the UK (7.7). Payment cards are used sparingly at the POS, and are primarily used to withdraw cash from ATMs.

As a result, alternative payment methods are sharply limited in terms of both usage and consumer interest. The only major area of the German payments market in which alternative and emerging payment tools have gained any traction is e-commerce.

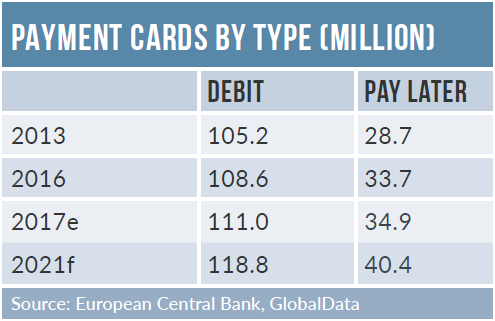

German consumers use debit cards for most transactions. National debit card scheme Girocard is the most frequently used payment card. Guarantees to retailers by all participating banks make Girocard popular among retailers.

Until a cap implemented by the EU in 2015, Girocard’s lower interchange fees compared to international schemes gave it an edge. The new interchange fee rules have, so far, had a minimal impact on its dominance in Germany.

Pay-later cards are not very popular in Germany, mainly due to a cultural aversion to debt. Credit cards represented only 2.1% and 1.4% in terms of card transaction volume and value respectively in 2017, and almost 70% of credit card holders paid off their balances in full each month.

The opportunity for credit card revenue in Germany is therefore limited, and there would need to be a seismic shift in the German attitudes to debt to change this.

Germany is the third-largest e-commerce market in Europe, behind only the UK (€175.6bn ($216.1bn)) and France (€81.1bn), although its population is much larger than both these countries. This indicates that Germans are not nearly as engaged with the online channel as French or UK consumers.

E-commerce’s growth in Germany has been facilitated by high internet and smartphone penetration, and the availability of fast broadband connections. Use of video and social media to enhance product presentation and services in e-commerce is further fuelling growth.

Compared to other European markets, payment cards are used infrequently, while online tools that hide the user’s payment details from the merchant – such as Sofort and PayPal – are more popular, driven by German consumers’ perception of these tools as both convenient and secure.