Iran’s payment card market recorded robust growth in terms of the number of cards in circulation, transaction volume, and value between 2013 and 2017, primarily supported by government initiatives to encourage electronic payments and reduce consumer dependence on cash.

Consumers are now charged a fee for using cash to pay utility and mobile bills. In addition, many banks refuse to accept bill payments in cash, requiring consumers to use cards, and have installed barcode readers and POS terminals in branches to facilitate this.

Go deeper with GlobalData

Furthermore, many government organisations pay bonuses to employees in the form of gift cards, which can only be used to make purchases and not to withdraw cash. These initiatives have also led to an overall increase in Iran’s banked population. Consequently, the percentage of the population aged 15 or above with a bank account rose from 87.2% in 2013 to 95.8% in 2017.

The gradual adoption of contactless technology, supported by the increased availability of various alternative payment methods, is likely to drive the Iranian payment card market’s growth in the near future.

Debit cards dominate

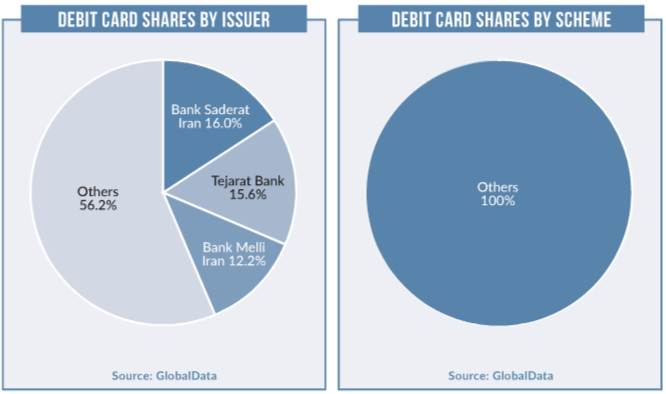

Debit cards accounted for 99.5% of the payment card transaction volume, and 99.4% of the transaction value in 2017.

Consumer preference for debt-free payments and prudent consumer spending habits have resulted in the dominance of debit cards in terms of both transaction volume and value. Growth was also supported by government efforts to encourage retailers to accept card-based payments, and banks’ promotional activities to encourage retailers to install POS terminals.

US Tariffs are shifting - will you react or anticipate?

Don’t let policy changes catch you off guard. Stay proactive with real-time data and expert analysis.

By GlobalDataDebit cards will continue to lead the Iranian payment card market, supported by the gradual migration of low-value cash payments to payment cards.

Pay-later card adoption

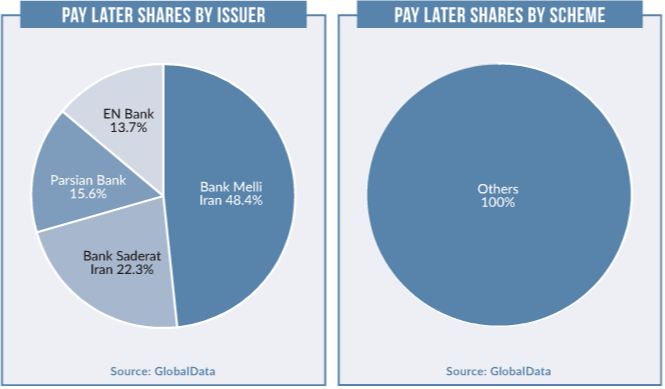

While debit cards remain the dominant payment card type, consumer adoption and use of pay-later cards is growing at a brisk pace, primarily supported by a number of initiatives launched by the Iranian government.

Targeting low-income individuals, in April 2017 the government introduced a scheme called Yarakart, which enabled banks such as Bank Keshavarzi and Iran Post Bank to issue credit cards for the lower-income sector of the population.

Similarly, in April 2018 the government announced the launch of a new credit card project that will allow banks to offer credit card loans at lower interest rates for purchases of Iranian products.

International sanctions

The lifting of international sanctions against Iran is expected to encourage more foreign banks to expand operations there.

In 2016, following the implementation of the Joint Comprehensive Plan of Action for the development of Iran’s banking system, the Central Bank of the Republic of Iran (CBI) partnered with numerous banks from countries including France, Austria, India, China, South Korea, Japan, Russia and Turkey.

In August 2017, the CBI announced the integration of the local Shetab and Russian Mir card networks, which will allow Iranian payment cards to be used at Russian ATMs and vice versa.

Robust prepaid growth

There is substantial demand for prepaid gift cards in Iran, in both the retail and corporate markets, with demand particularly high during festival seasons.

All major banks, such as Keshavarzi Bank, EN Bank, Pasargad Bank and Bank Melli Iran, offer gift cards, which can be obtained for retail and corporate customers without an account.

To take advantage of the growing e-commerce market, banks such as Bank Mellat, EN Bank, Bank Pasargad and Parsian Bank offer prepaid cards for online shoppers, encouraging customers to use e-banking services to pay for utility bills and online shopping. As an example, Bank Mellat offers a prepaid card that can be used for online shopping and to pay utility bills.

It features a three-digit CVV code, and the card is deactivated if the code is entered incorrectly three consecutive times.

Card acceptance at POS

The number of POS terminals recorded a CAGR of 18.3% between 2013 and 2017, and is anticipated to reach 8.6 million by 2021.

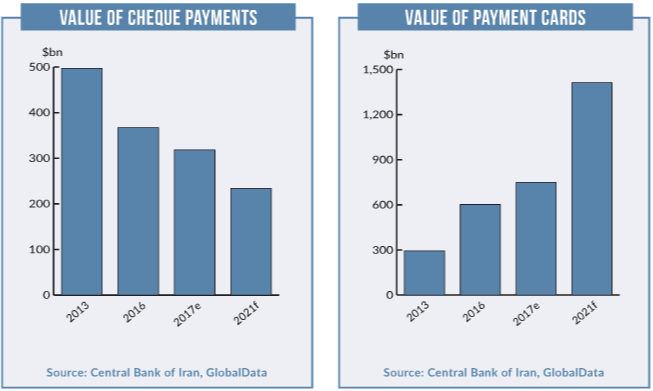

The transaction volume at POS terminals increased significantly from 5.6 billion in 2013 to 16 billion in 2017, at a CAGR of 30.2%, while the transaction value increased from IRR10.6bn ($294.38bn) in 2013 to $749.67bn in 2017 at a CAGR of 26.3%. Contactless POS terminals are also gaining prominence in the country.

According to Tehran-based payment solution provider Sadad, the company has installed 650,000 POS terminals in Iran, of which 150,000 are equipped with NFC technology.