The UK payments market is highly mature – arguably even overserved by its financial institutions.

Go deeper with GlobalData

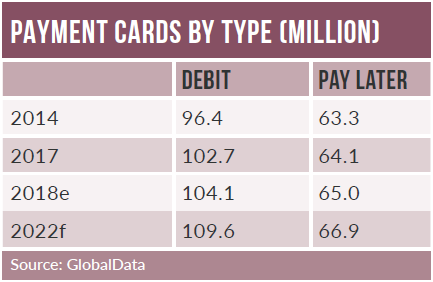

There were more debit cards in circulation than individuals in the UK in 2018, by a considerable margin. Access to formal financial services in the UK is easy and mostly free, leading to a population that is highly comfortable with credit and debit cards, both in-store and online.

Contactless card numbers and use have also seen strong growth in recent years, with the vast majority of contactless users in the UK seeing the cards as helpful. Indeed, widespread adoption of contactless – backed by strong infrastructure – is anticipated to further drive electronic payments in the country.

A range of card-issuing and alternative payment brands covering e-commerce and mobile proximity payments are available, including Apple Pay, Samsung Pay and Google Pay. However, there are notable areas of weakness: the mobile proximity payments market in particular is still underdeveloped, and many UK consumers still prefer cash to a certain extent. The Brexit referendum result also leaves the future of the UK payment market unclear.

Rising pressure on profitability and growing consumer preference for online banking are driving digital-only banks in the UK. Atom Bank was the first such bank, and this model is also used by Starling Bank, Monzo and Fidor Bank.

In September 2018, Goldman Sachs’s digital bank, Marcus, was launched in the UK, followed by Germany-based digital bank N26 in October, allowing customers to carry out all banking tasks 24/7 from any location. The proliferation of digital-only banks is likely to further heighten competition in the banking space.

Contactless payments are growing in popularity due to retailers’ extensive deployment of contactless POS terminals, coupled with backing from the big banks and consumer enthusiasm for the convenience of contactless.

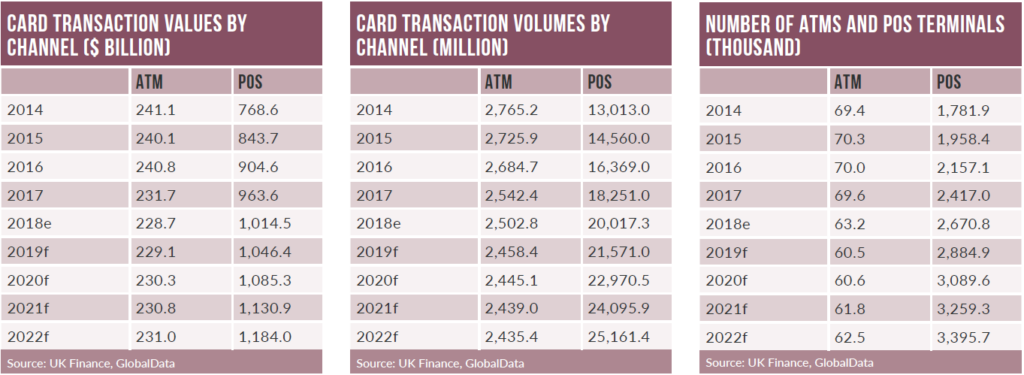

According to UK Finance, there were 118.9 million contactless cards in circulation as of December 2017, up from 58.7 million in 2014. The number of contactless payments made in the UK rose by 97% during 2017 to 5.6 billion. These consisted of 4.9 billion contactless debit card payments and 0.7 billion contactless credit card payments.

The e-commerce market value registered robust growth from £103.4bn ($131.9bn) in 2014 to $212.3bn in 2018, driven by growing internet and smartphone penetration. Online shopping events such as Black Friday and Cyber Monday also helped boost e-commerce sales.

The UK e-commerce market is led by payment cards, with debit and credit cards accounting for nearly 49% of all online spending. PayPal, the third-most-popular online payment tool, is also mainly funded by payment cards, with convenience and security being key factors.