One of the countries embracing digital payments the most eagerly is Canada. Consumers have a desire to pay differently and more conveniently, so how is the market responding? Briony Richter reports

The rise of digital technology in payments – from smartphones and wearable devices to artificial intelligence – is rapidly transforming how consumers in Canada want to pay.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

However, friction at the checkout service is causing more Canadian shoppers to abandon purchases altogether. The Payments Pulse Survey: Consumer Edition details the results of research conducted by Leger Marketing and Payments Canada, which analysed the various and emerging payment habits of Canadian consumers.

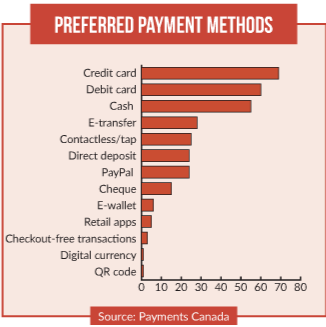

It noted that Canadians are increasingly adopting digital solutions. While the top three forms of payment are credit cards, debit cards and cash, the research also suggested that around 55% of Canadians are willing to give up cash altogether.

Gerry Gaetz, president and CEO of Payments Canada, says: “The high abandonment rates at checkout suggest there is a high cost of not integrating faster, more convenient payment technologies. Canadian consumers are speaking with their wallets, indicating that they will not buy from those businesses that don’t make the payment experience easy.”

Overall, Canadians prefer credit and debit cards as their main payment method. Of all the payment options, 69% of those surveyed stated that they use a credit card more frequently; coming in second are debit cards at 60%.

Two-thirds (67%) of Canadians use a credit card for monthly payments. Loyalty rewards also account for a large amount of credit card payments, with three in four (74%) saying they use their credit card to collect rewards.

The reason for credit card usage is divided between generations. Canadians aged between 18 and 44 are significantly more likely to use a credit card for monthly payments, as this is likely to build up a credit history. On the other hand, Canadians aged over 35 are more likely to use a credit card to earn rewards.

Although physical cards are still extremely popular, Canadian consumers living in cities are particularly enticed by the notion of invisible payments. In urban neighbourhoods, consumers are more interested in payments becoming more invisible (49%) than those living in suburban (42%) or rural (31%) areas where dependency on cash and physical cards tends to be greater.

Overall, 43% of Canadians are interested in invisible or non-checkout payments in store,

and platforms such as Amazon Go, AliPay and WeChat Pay all offer frictionless checkout processes. Invisible payments technology will significantly reduce the number of abandoned checkout purchases in Canada; coupled with enhanced security, it gives customers peace of mind and an added level of convenience while banking and shopping on a daily basis.

Canada payments: Rise of digital payment methods

While the traditional methods are still more popular in mature markets such as the US and Canada, alternative digital payments are growing fast.

The Canadian payments industry in particular is witnessing a shift towards digital. Paying with a mobile devices and downloading e-wallets are fast becoming very popular.

According to the Payments Pulse Survey: Consumer Edition, four in 10 Canadians store personal credit card information with a mobile app or online e-commerce site, and the vast majority (86%) feel confident that the app or service provider they are using ensures the security and privacy of their personal credit card information.

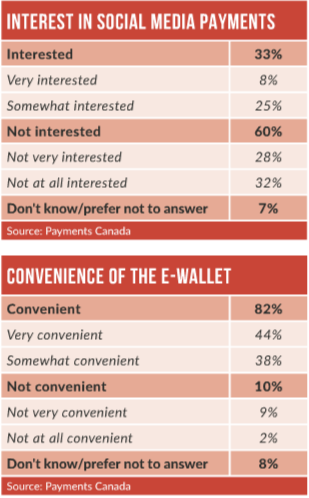

The survey also noted the traction that e-wallets are gaining among Canadian consumers. Of those surveyed, 70% of Canadians who have uploaded an e-wallet have used this payment type at least once since its launch in Canada.

On the rise of digital payment methods in Canada, Gaetz notes: “With record levels of overseas travel, many Canadians are getting a taste for new, more convenient digital payment platforms, and are expecting to see these technologies roll out in Canada as well.

“Fortunately, we are working with Canadian financial institutions and key government stakeholders to design and implement new payment systems, rules and standards that will make it possible to introduce faster, safer and more data-rich payment options for Canada’s businesses and consumers.”

Social media

Social media platforms have significantly larger customer bases than any bank.

What started out as stages for connecting people across the globe have steadily transformed into business tools that are now consumed by various advertising and promotional campaigns.

The next step in the social media space is the implementation of a payments gateway. Quick, accessible and convenient, placing payments within platforms such as Facebook, Alipa and Twitter could substantially reshape the whole sector.

The trend is steadily catching, but mostly among the millennial generation. Those aged 18-44, predominantly male and living in urban cities are significantly more on board with the idea of paying through social media.

Overall, the emerging payments innovation still has a way to go, however, as one-third (33%) of Canadians are interested in social networking apps, such as Alipay and WeChat, as a payment option in Canada, while 60% have no interest at all.

Cheques are out

The days of the reliable cheque book seem numbered. With so many different ways to pay, it is not too hard to see why cheques are becoming antique in the payments sphere – in Canada, in particular, it is ‘plastic fantastic’.

While the age of cheques may be coming to a close, the number of debit and credit card transactions in Canada have sky-rocketed. However, there are still Canadians writing cheques, and the Canadian government has made attempts to bring them into the digital age.

Remote deposit capture or cheque scanning is widely used across Canada, with more than 20 Canadian financial institutions offering mobile cheque deposits to customers. On average, Canadians write three cheques a month, with an average monthly value of just under C$250.

On the other hand, 40% of Canadians do not write cheques at all, and of those that still do, around 66% want to move to a more convenient method. There are a number of drawbacks with cheques. Debit cards and e-wallets are far quicker and can be used at any time, whereas the long clearing cycle of a cheque means the recipient could be waiting days before the transfer clears.

For Canadian millennials, the jury has already returned a verdict: the vast majority do not even own a chequebook, and those that do are significantly more likely to switch to a digital option. The invasion of digital technologies is certainly reshaping the Canadian payments sector.

In the coming years, mobile and e-wallets will almost certainly take off, although whether paying through social media will become the norm is yet to be seem. However, the market is constantly evolving, and will continue to test and adopt more innovate payment solutions.