Danske Bank has launched FastPay its new wearable offering. With the Nordic region embracing cashless, this offering should perform well. However, is it too little too late? Do Nordic consumers need this option? Patrick Brusnahan writes

Wearable technology is all the rage. With Fitbit Pay and Garmin Pay available across multiple markets, payments have entered the space. This isn’t even considering the smart watches from Apple, Samsung and other tech giants.

Go deeper with GlobalData

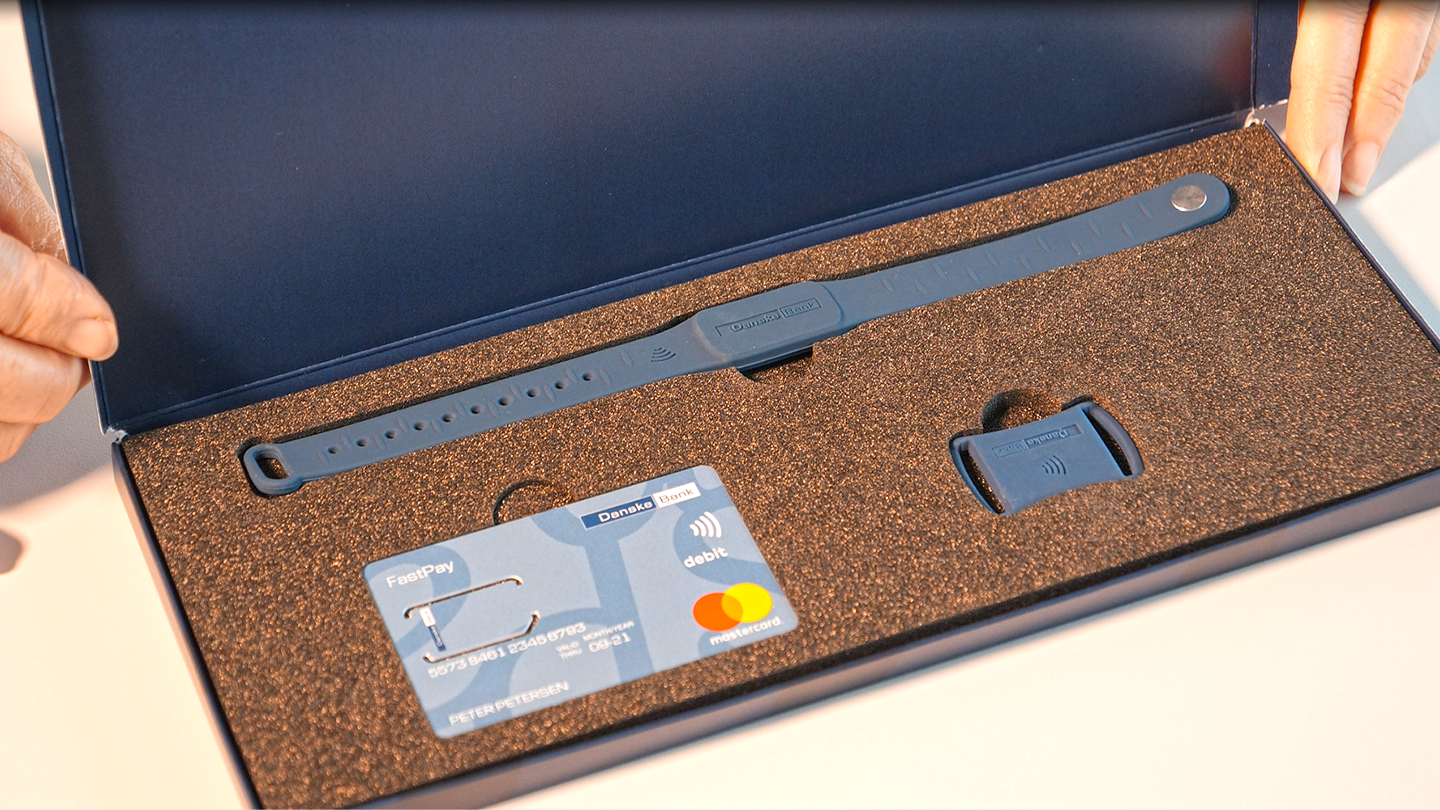

Danske Bank has decided to enter this ring. FastPay is the lender’s new payment solution. It lets you wear a payment chip in a wristband, key ring, or watchstrap. It allows contactless payments without the customer rummaging through their pockets to find their card.

Launched across Denmark, Norway, and Sweden from October 2018, it wants to be a supplement to Danske’s other solutions, such as MobilePay.

Wearables

Cash is now used in less than 20% of Swedish retail payment transactions, according to the Riksbank, Sweden’s central bank. Most Swedish retailers and transport companies decline to accept cash, with cash payments now totalling 2% of total payment transactions. Around 900 of Sweden’s 1,600 bank branches no longer hold cash or accept cash deposits, and many branches, especially in rural areas, do not offer ATMs.

There are several success factors in Sweden’s move to digital payments. For example, the widespread adoption of Bank ID, a bank-based digital identification and signature system that currently has 7.5 million users in Sweden.

Denmark and Norway have similar BankID coalition digital ID schemes that are used for e-commerce, banking and government transactions.

Morten Schwaner, head of card and mobile payments at Danske Bank, believes wearables are a great opportunity.

Speaking to CI, he says: “We see an opportunity. Contactless has been moving quickly in the Nordic markets, especially in Denmark. People are very keen on trying new ways of paying. The solutions we have, such as the different wallet solutions, all require technical health in some way in the form of a technical device. This form of wearables is free for everybody to use, it doesn’t require a specific technical device.

“Then of course, there is the ease and the fast way of paying.”

Currently, it’s only in its pilot stage, but Schwaner is optimistic about its chances.

He explains: “We are starting out with a pilot to whom we will invite a couple of thousand customers to try it out. We will gather insights and hear about how they feel about the solution and then we can see what is good and what we need to improve on before we go live in the market with the final product.”

Danske wearables: the future?

While this product could be branded towards younger, more technologically-savvy consumers, as a lot of new tech are, Schwaner thinks its potential is much larger. He feels there is no need to limi its target market.

“We actually think that this could be available for any type of customer from children to the elderly,” he explains. “That’s one of the things we are very keen on trying out in the pilot, to have people of different age groups testing it out. We don’t have a particular segment in mind.”

One thing that is not yet decided about the offering is pricing. At the moment, it may depend on what type of customer is using it. However, it may also be packaged together with other products.

Similar products have been launched in the UK. Barclaycard’s wearable brand, bPay, was trialled in 2012. Three years later, it launched three payment products – a fob, a wristband, and a sticker. Since then, it has moved into fashion, jewellery and expensive timepieces.

There are options out there, so what will help FastPay stand out? Surely, as Scandinavia is a nearly totally cashless region anyway, the customer already has a preferred solution. I it too late for Dasnske bank to make a dent?

Schwaner concludes: “We’ve had Fitbit Pay for almost a year now [in Sweden] and Garmin Pay since February and we haven’t seen a large number of customers using it. We don’t think there are that many that are using these solutions yet. That’s why we think that opening something that is available for everybody is worthwhile.”