Covid-19 will turn out to be a tipping point for digital payments. Mohamed Dabo set out to find out about the ‘new normal’ for the fintech and payment sectors.

It’s too soon to guess when the coronavirus will abate, or for how long, or the duration and depth of the current economic downturn. What’s clear, though, is that payments systems have entered a new phase of digital innovation.

Go deeper with GlobalData

The pandemic has ushered into the marketplace a bigger, structural change—the transition to digital payments—which is likely to continue when the economy eventually recovers.

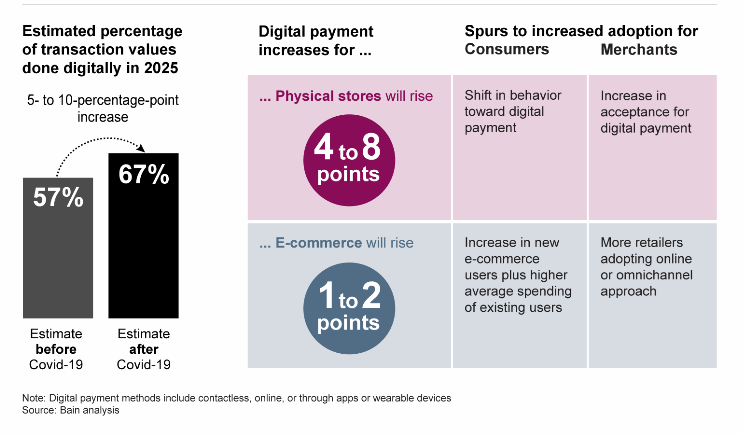

By 2025, the adoption of digital payments could accelerate by 5 percentage points to 10 percentage points globally, above what was previously anticipated, according to data from management consulting firm Baine & Company.

Covid-19 is spurring faster adoption of digital payments

Source: Baine & Company

Source: Baine & Company

The magnitude of the pandemic’s effects will differ depending on a company’s position on the payment value chain and its customer base.

How well do you really know your competitors?

Access the most comprehensive Company Profiles on the market, powered by GlobalData. Save hours of research. Gain competitive edge.

Thank you!

Your download email will arrive shortly

Not ready to buy yet? Download a free sample

We are confident about the unique quality of our Company Profiles. However, we want you to make the most beneficial decision for your business, so we offer a free sample that you can download by submitting the below form

By GlobalDataYet as consumers and merchants speed up their adoption of digital payments, all providers will have to find ways to strengthen their customer relationships, so that they get their fair share of the market.

Fintech: the unlevelled playing field?

In the case of e-commerce, social media and alternative technologies, some companies are thriving and a few players are consolidating their position.

This can be seen in the banking sector too, where government programs are primarily distributed through incumbent institutions. For example, while PayPal and Square received permission in the US to distribute funds, neobanks did not.

This furthers the perception, and probable reality, that powerful firms will not only remain powerful but are growing. In the US alone, billionaires have added $380bn to personal wealth, while unemployment claims skyrocket.

In the banking sector, there are two main points of pain: customer engagement and business performance management.

Banks have been pushed to engage with consumers to drive better customer experiences and have been looking to leverage fintech partnerships or acquisitions to do just that.

As the Covid-19 crisis continues, many of these projects have been put on hold in favour of other major topics for banks, such as enabling staff to work from home (which is operationally very hard), ensuring access to core systems (i.e., money and credit) as well as managing own company costs and operating pressures.

We now see a massive shift in focus at banks from fintech for customers to fintech for the business and its systems.

New challenges and opportunities

The covid-19 pandemic continues to impact most industries at an unprecedented scale globally. What does it all mean for the fintech and payment sectors?

Will the covid-19 crisis accelerate an existing trend towards the widespread uptake of smart financial tools? Or will these sectors—like some others—find themselves crippled by the financial and social shock of the epidemic? And will startups be particularly vulnerable?

According to a new report published by Amsterdam-based fintech investor, Finch Capital, the fintech sector in general will face some real difficulties over the next few months. While the post-crisis outlook seems to be positive for many businesses, others will struggle to regain any momentum that has been built up so far.

As for the payment sector, the surge in digitisation, expected by many to continue post-covid, will naturally be beneficial. Many believe the number of digital transactions relative to physical cash transactions will continue to rise after the pandemic.

The decline of cash?

“It is probably too early for the data to tell us this, but most of us in the payments space are certain that this is the case,” says Santosh Tripathy, practice lead, digital payments with financial transaction management company SmartStream Technologies. “In this environment, cash is losing its shine,” he says.

This could be the push needed for many countries to become truly cashless.

“It’s no longer inconceivable for entire countries to run on digital cash – we are already seeing this play out,” says Victor Penna, global head of treasury solutions at Standard Chartered.

“Most people have access to a mobile phone – which can also act as a digital wallet – and a number of central banks are thinking about introducing digital currencies. This is how we can boost financial inclusion and support the most vulnerable in society,” he added.

“One good thing to come out of this crisis is that I think more and more economies will start going cashless,” says Kohli.