PayU Launches LazyCard to Tap into India’s BNPL Market

India-based fintech PayU is rolling out LazyCard from LazyPay to tap into the growing popularity of Buy Now Pay Later, writes Douglas Blakey

PayU is eyeing up a clear gap in the Indian credit market with a mere four in every 100 Indians holding a credit card. While PayU’s stated ambition to revolutionise the way Indians access credit will be far from easy to execute in practice, it can take heart from the prudent manner in which Indian consumers manage their credit card accounts.

Go deeper with GlobalData

LazyPay is throwing itself with gusto into the Indian card segment with the launch of LazyCard. The goal is simple to summarise: to empower India’s underserved with access to credit. In partnership with SBM Bank India and Visa-branded, LazyCard incorporates a strong rewards structure.

The aim, says LazyPay: “is to to create value for customers in every transaction by offering bigger, better cash back rewards and offers like never before.” Digitally linked to the LazyPay app the card launch also flags up robust technology to ensure security and a hassle-free experience in managing payments.

The card is available to 62 million pre-approved users of LazyPay. Specifically, LazyPay offers customers a credit limit of up to a maximum of INR500,000 ($6,645). Other selling points include no joining fee and no annual fee for cardholders.

BNPL gains traction in India

Buy now pay later is gradually gaining traction in the Indian payment market, with an increasing number of merchants, banks, and payment providers now offering the service. In January 2017, Flipkart introduced an option that allows customers to purchase goods up to a total value of INR10,000, which can be repaid at the end of the credit cycle without any charge. International companies are also planning to enter the market. In August 2020, US-based buy now pay later provider Sezzle announced plans to enter the Indian market.

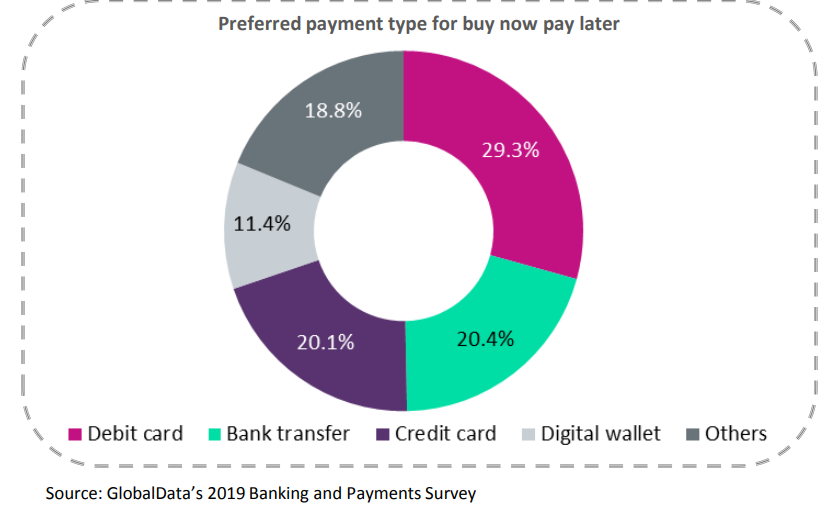

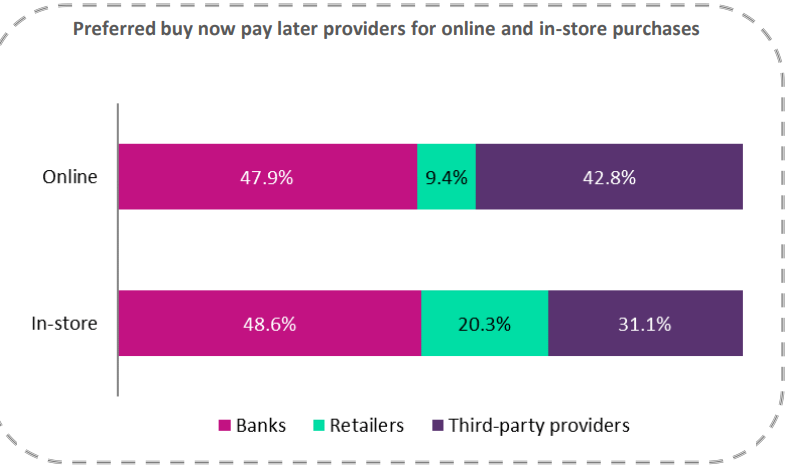

GlobalData research reveals that some 57.2% of Indian consumers use BNPL for online purchases. Around 43.5% use BNPL for in-store purchases.

But it is cash that continues to dominate the payments landscape in India, accounting for 75.2% of overall payment transaction volume in 2020. However, as a result of government initiatives, bank efforts, and growing consumer confidence in digital payments, Indians are gradually shifting towards electronic payments.

GlobalData research estimates debit card payment turnover in India at a modest $160 in 2020, trailing its peers China ($1,231), Malaysia ($302), the Philippines ($262), Vietnam ($203) but ahead of Cambodia ($154), Indonesia ($116), Thailand ($92), and Pakistan ($56).

PayU believes it can grow its BNPL offering at pace given the low credit card penetration rate of about 4.6 cards per 100 individuals in 2020. However, with improved credit bureau standards and retail borrower behaviour, as well as rising consumer disposable income, banks have become more confident about credit card issuance. Both public and private sector banks offer credit cards to individuals with no prior banking relationships. While credit and charge cards have lower adoption compared to debit cards, they still account for 47.5% of total card payment value in 2020.

GlobalData research: the India credit card market

Credit and charge card payment frequency in India is estimated at 38.6 transactions per card in 2020, compared to China (66.0), Malaysia (52.0), the Philippines (34.8), Thailand (26.8), Pakistan (24.7), Indonesia (19.5), Vietnam (12.8), and Cambodia (7.9).

In 2020, credit and charge card payment turnover in India is estimated at $1,865, compared to China ($9,151), Malaysia ($3,726), the Philippines ($2,431), Thailand ($2,404), Indonesia ($1,397), Vietnam ($1,115), Pakistan ($872), and Cambodia ($859).

To further promote card usage, credit card issuers offer value-added benefits such as reward points, annual fee waivers, and discounts.

Indian credit card holders are noticeably price-sensitive. They are motivated by reward points, cashback, and low annual fees. So it is notable that PayU is also offering users rewards on every transaction.

Users have an opportunity to earn 1% to 5% cash back on every transaction. PayU says that this makes it one of the most rewarding cards available in the market.

A massive credit gap

Prashanth Ranganathan, CEO, PayU Finance, says: “As per various industry reports, today only about 3 in every 100 Indians owns a credit card, creating a massive credit gap in our economy. We are excited to launch ‘LazyCard’, to empower and elevate the underserved, by giving them means to carry out financial transactions without worrying about their bank account balance.

“Backed by our proprietary credit underwriting capabilities and data science muscle, the card boasts the largest pre-approval base of 62 million customers, helping more people qualify, particularly in the pandemic’s strenuous economy. We aim to reach corners of the population and give a card in the hands of all underserved Indians.”

Moreover, Pay says that its LazyCard ‘Booster’ feature is useful for thin-file borrowers to rebuild their credit score or establish their credit history. This feature enables users to get access to the card by setting up a fixed deposit with RBI-regulated SBM Bank India in a fully digitised two-minute app flow. ‘Booster’ feature allows users to get three benefits (1) Money security via fixed deposit, with higher interest rates than savings for boosting wealth (2) Cashbacks & offers on LazyCard that boosts the credit line (3) Improve credit score over time to strengthen their eligibility for future credit needs. As the user continues to transact using the card and build up creditworthiness, LazyPay will start unlocking the credit line. The user is then free to withdraw the deposit and continue enjoying access to enhanced credit and rewards on the card.

India growth of digital payments without a PoS

A growing number of companies are offering innovative payment solutions to SMEs and micro merchants, enabling them to accept digital payments at low costs. Financial services companies such as ftcash, Instamojo, Paytm, PayUnow, and Razorpay enable merchants to accept digital payments for in-store sales. They create a unique payment link for the merchant, which can be shared with customers via Facebook, WhatsApp, SMS, or email. Customers need to click on the payment link to make payments for their purchases.

Neeraj Sinha, Head – Retail & Consumer Banking, SBM Bank India adds: “There is a need to solve for the credit needs using Smartbanking solutions that are available, accessible, and affordable. SBM Bank India is endeavouring, as a part of its comprehensive SmartBanking solution set, in partnership with LazyPay, to introduce the Visa powered LazyCard.

“Further this Card will smoothen the entire loan processing capability at LazyPay’s end thus helping to bring them towards better financial inclusion. We are elated to partner with LazyPay towards this prepaid card.”

Fintechs at the heart of innovation, driving financial inclusion

Sujai Raina, Head – Business Development, India, Visa, says: “Fintechs like PayU Finance have, in recent years, been at the forefront of driving innovation and financial inclusion of new consumer segments in India. We are excited to launch the LazyCard programme to make credit more accessible to existing LazyPay customers as well as new-to-credit users.

“This Visa-powered LazyCard is issued instantly, available in physical and virtual form, and offers users a readily available credit line, rewards and Visa Platinum benefits, enabling seamless and secure payments across millions of merchants that accept Visa cards.”

Potential for BNPL user numbers growth and the bad debt challenge

Inherent in the launch of the BNPL product offering is the risk of default. PayU can however take some comfort from the credit card sector-providing they optimise the credit scoring challenge.

For example, over seven in 10 Indian credit card holders repay their outstanding credit card balance at the end of each month.

The average Indian consumer owed INR883 on credit cards in 2020. The average balance owed per credit card is around INR19,346.

In terms of current users, estimates vary but there are currently around 10 million Indian consumers using BNPL. The most optimistic local analysts believe that this number can grow to around 80 million or even 100 million within five years. If and it is a big if such estimates prove to be accurate and if issuers such as PayU can keep on top of the bad debts challenge, then they may just be able to achieve the goal of revolutionising the local credit market.