The Monetary Authority Singapore (MAS) is forward-thinking in its approach to innovation and technology. At the end of 2016 the regulator teamed up with banks and the R3 consortium to investigate the use of Distributed Ledger Technology (DLT). Anna Milne highlights the key points from the project report

Project Ubin was implemented with the chief aim of reducing risk and cost for cross-border settlements of payments and securities in Singapore, primarily through the use of cryptocurrency.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

Announced in November 2016, it was a proof-of-concept project between the Monetary Authority Singapore (MAS), R3 and a consortium of financial institutions to conduct interbank payments using blockchain technology. Partner banks include Bank of America Merrill Lynch, Credit Suisse, DBS Bank, HSBC, JP Morgan, Mitsubishi MFG Group, OCBC Bank, Singapore Exchange and UOB Bank, with BCS Information Systems providing the technology.

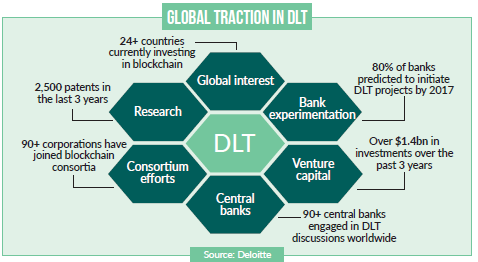

The World Economic Forum 2016 report The Future of Financial Infrastructure, produced in collaboration with Deloitte, predicted that 80% of banks would initiate DLT projects in 2017, the driving force behind these ventures being to reduce the significant cost, risk and friction of existing financial services infrastructure.

Antony Lewis, director of research, R3, and co-author of the Project Ubin report, wrote a piece, separate of the MAS project, explaining the “compelling reason to decentralise as much critical financial and digital infrastructure as possible,” and that reason is cyberwar.

Project Ubin aimed to place a tokenised version of the Singaporean dollar (SGD) on a distributed ledger, with each token fully backed up by fiat currency, i.e. a depository receipt model.

Based on Deloitte’s research, these three innovations were core to DLT’s invention:

- Peer-to-peer networks: Each peer in the network is a server and client, both supplying and consuming resources. This could facilitate the creation of a currency without a privileged third party, amongst other types of decentralised financial interactions. This enables the facilitation of transactions without a central, privileged third party, even in the absence of trust.

- Public key cryptography: This is a method for verifying digital identity with a high degree of confidence. Public and private keys consist of a sequence of random numbers – a numeric code. This allows for increased security and protection of data and identity in the system.

- Consensus: Consensus algorithms that ensure agreement between two parties on a network can help validate the data’s authenticity as well as transactions and control when it can be written into the system. This capability prevents double spending by ensuring chronological recording of data. This enables the secure automation of complex, logical agreements and the business processes using data gathered by Oracles.

FURTHER BENEFITS

The immutability of data on the network makes it resistant to double-spending, fraud, censorship and hacking, creating a more secure, transparent network and new avenues for regulators. Real-time settlement is another attractive feature of distributed ledgers, as it removes friction and risk.

The first phase of Ubin was to assess the feasibility and implications of DLT and to identify the elements required for future enhancements, in the main to identify its feasibility and benefit to the real-time payments system. As part of this investigative process, the project used the MAS MEPS+ system to enable real-time fund transfers to issue funds on a DLT.

When considering the risks and inefficiencies within cross border transactions, Project Ubin could do well to put some of these to bed:

- Replacement risk, when a counterparty cancels or delivers late;

- Settlement risk, when a counterparty defaults; the precautionary measure of funding costs, where parties on both sides of a transaction pre-fund accounts early, safeguarding against a worst-case scenario, and

- Reconciliation costs, which are multi-way and required across payments and securities to understand real-time stock position.

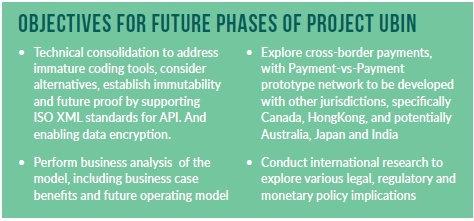

Phase 2 and beyond will involve developing real-world applications based on the prototypes created in Phase 1. It will provide opportunities for students and working professionals to get involved in app development, and spin-off projects will have a focus on cross-border payments and securities transactions.

The SGD-on-ledger is a specific-use coupon issued on a one-to-one basis in exchange for money. The coupons have a specific usage domain – in this case the settlement of interbank debts – but no value outside this. The coupons are exchangeable into cash at a later point. Each token is fully backed by the equivalent value in real SGD, meaning the overall money supply is unaffected by the issuance of the on-ledger dollar movements.

The prototype, built on the Ethereum platform, integrated both Ripple and Stellar blockchain platforms, enabling P2P transactions across geographies. Also, crucially, the ledger holdings do not gain interest-reducing the complexity of managing the payment system.

Deloitte has built over 30 blockchain proofs of concept and prototypes for industries including consumer and industrial products, financial services, life sciences and healthcare, plus other cross-industry applications.

Singapore is renowned for fintech innovation. If Project Ubin turned out to be a success, it would be the first Asian digital currency. One key factor to address in order to bring it to fruition would be the underlying legality of the system. Furthermore, a future phase would experiment with banks being able to borrow digital SGD from each other without posting cash with MAS.

Will it work? The key is to differentiate between a decentralised real-time gross settlement system and a central bank digital currency – the former being a background process and a system to which the general public would not be privy.

To this end, it makes a great deal of sense. The question is whether blockchain technology is capable of doing what so many claim is possible with it. And certainly there are many sceptics. MAS and R3 should have an answer for us soon.