India’s vibrant payments ecosystem is expanding and evolving. Digital platforms such as mobile wallets, payments banks and electronic authentication are all experiencing explosive growth.

The volume of digital transactions in the country grew from 32% in 2013-14 to 62% in 2017-18. Behind the dramatic growth of the sector are dynamic factors that are driving the payments sector into the future.

How well do you really know your competitors?

Access the most comprehensive Company Profiles on the market, powered by GlobalData. Save hours of research. Gain competitive edge.

Thank you!

Your download email will arrive shortly

Not ready to buy yet? Download a free sample

We are confident about the unique quality of our Company Profiles. However, we want you to make the most beneficial decision for your business, so we offer a free sample that you can download by submitting the below form

By GlobalDataThe rise of digital India

India is one of the largest and fastestgrowing markets for digital consumers. As digital capabilities improve and connectivity becomes omnipresent, technology is poised to quickly and radically change nearly every sector of India’s economy.

The runaway digitisation is expected to further accelerate the penetration of digital payments, with a number of key areas standing out:

Rising mobile penetration

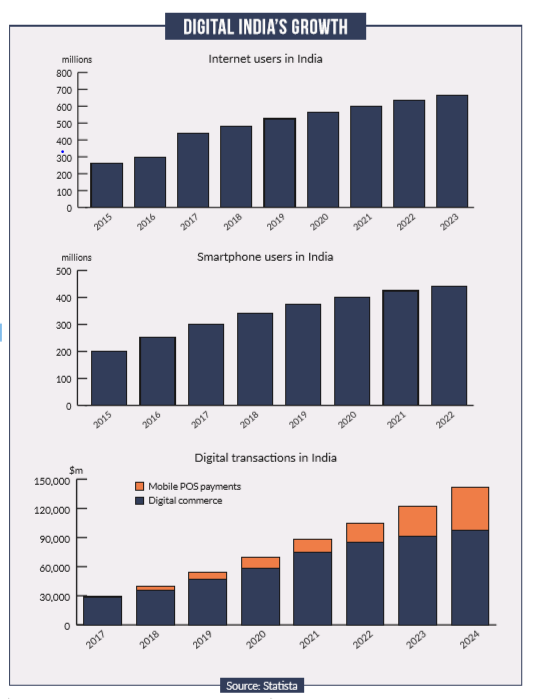

India currently boasts the second-fastest rate of mobile penetration in the world, with more than one billion subscriptions. German online statistics platform Statista predicts that by 2022, 36% of mobile phone users in the country will use a smartphone, up from 26% in 2018 (see chart).

Growing internet use

India had 560 million internet subscribers in September 2018, second only to China. Digital services are growing in parallel.

Indians download more apps – 12.3 billion in 2018 – than any country except China, and spend more time on social media – an average of 17 hours a week – than social media users in China and the US.

The share of Indian adults with at least one digital financial account has more than doubled since 2011 to 80%, thanks in large part to the government’s mass financialinclusion programme, Jan-Dhan Yojana.

Soaring digital transaction numbers

The total transaction value in the digital payments segment is projected to reach $69.2bn in 2020, and record a CAGR between 2020 and 2024 of 19.5%, resulting in a projected total amount of $141.3bn by 2024.

Supportive regulation

The Reserve Bank of India (RBI), India’s central bank, has said that the country’s payments sector needs strong and supportive regulation to grow rapidly and earn a leadership position in the world.

However, much remains to be done in this area. Local experts are firmly of the view that bringing down the volume of paper clearing, along with raising consumer acceptance of digital utility bill payments, is still a key challenge.

The following are examples of regulatory steps that are currently enabling digital payments in India:

The RBI has eased KYC rules for opening a bank account

The process of providing documentation to prove a customer’s identity and validate their address – to opening a bank account, for example – is becoming simpler.

Previously, the KYC process required the submission of separate proofs for address and identity. The RBI has done away with this; now, a single document with a photograph and address of the applicant will suffice. In a country as large as India, this potentially affects millions of customers.

RBI has waived two-factor authentication

The industry applauded the central bank’s decision to waive second-factor authentication or one-time passwords (OTPs) for transactions less than INR2,000 ($26.60).

This had been a long-standing demand of the industry, which felt that waiving OTPs for lower-value transactions would make them easier, and therefore would attract more people towards cashless transactions.

Unified Payment Interface (UPI)

UPI is a real-time interbank payment system that allows users to send or request money. Since launch, India’s UPI has hit a significant milestone of one billion transactions per month.

In September 2019, UPI clocked 955 million transactions, amounting to INR1.61trn, demonstrating the extent to which Indian consumers have exuberantly welcomed real-time payments.

Next-gen providers

India is now entering the next phase, where cheap data and faster connectivity are enabling those with a smartphone to access a new world of digital services. A new generation of payment service providers are emerging in response to rising customer expectations, with consumers increasingly demanding seamless transactions.

Indian customers are now more digitally literate, and have come to expect the convenience and speed of digital, whether shopping online or questioning a bill.

Consumer relationship has also become a differentiating factor. Leaders are 2.6 times more likely than bottom-quartile firms to use digital tools to manage customer relationships.

However, in the scramble the engage customers, smaller operators are fighting back. A recent survey found that 70% of small businesses use their own websites to

reach clients, compared with 82% of big companies.

Small businesses are less likely than big companies to buy display advertisements

on the web (37% versus 66%), but they are ahead of big companies in connecting with customers via social media, and more likely to use search-engine optimisation.